What Is the Law of Supply?

Law of supply is an important principle in economics which describes that there is a proportional relationship between product price and the quantity of product supplied in the market, assuming that factors that could affect this relationship remain unchanged.

That is to say, as the product price increases, the quantity of product supplied also increases. And as the price falls, the quantity supplied will consequently fall. This price-supply relationship in the law of supply determines how producers respond to price changes in a competitive market.

How the Law of Supply Works?

The law of supply can be implemented across most industries. It helps in explaining producer behavior and how they regulate the supply of goods in the market. As soon as the product price increases, the producers see an opportunity to make more profit by producing more of that product.

On the contrary, a consistent rise in prices can also hurt buyer sentiment. As a result, the demand of the product begins to fall, which in turn leads to the decrease in product price. Consequently, the suppliers will produce less and so the quantity supplied in the market decreases, following the law of supply.

Adjusting the production based on frequent price changes as dictated by the law of supply can be tricky, if not managed well. According to a study conducted by Gartner, 40% of the high-performing organizations are implementing automation to optimize their decision-making, which makes it significantly easier to regulate product supply in accordance with changes in product price.

What Factors Influence the Law of Supply?

1. Technological Advancement

Automation of critical functions with ERP software enables business owners to get total control over their company and enhance operational efficiency, helping them increase the supply of goods. Also, new production techniques and emerging technologies allow cost-effective production.

2. Resource Availability

A ready supply of raw materials plays a crucial role in ensuring continuity in production. ERP for electric vehicle manufacturing seamlessly manages suppliers and negotiation procedures, making it easy to manage the procurement of rare earth metals like lithium. However, skilled labor shortage can affect the supply.

3. Government Regulations

Complex and changing government regulations and compliances can be challenging to manage without business management software, thus influencing the supply of products. Moreover, unforeseen events like natural disasters and pandemics can impact the supply chain too.

4. Market Factors

Businesses base their production plans on forecasts of future demand and pricing. An ERP system can help businesses improve demand forecasts by considering factors such as economic growth and seasonal variations. Also, new suppliers may enter the market even if prices are not increasing and demand is stable.

5. Production Costs

The cost of production can significantly rise due to an increase in labor and raw material costs. Frequent breakdowns and faulty production can also impact production. A regular maintenance repair and overhaul not only ensures that the cost of production is in control but also prevents downtime in operations.

You May Like: What are the main Features of Supply Chain Management?

What are the Types of Supply?

There are five types of supply. Let’s discuss each of them.

1. Joint Supply

Joint supply is a type of supply where there is a production of multiple products from a common production process or resource. The quantity of multiple products supplied is dependent on each other, like petrol and diesel, which rely on a common process of oil refining.

2. Composite Supply

This type of supply is when a secondary product or products are supplied along with the primary product and the supply of secondary products is dependent on the primary supply. For example, ERP implementation can only happen if there is proper IT infrastructure and hardware available to run it.

3. Short-Term Supply

In short-term supply, the product being supplied is only available for a limited period, limited by its current production capacity. For example, irrigation water can be in short supply during the dry season, where solutions like Agriculture ERP come in handy to manage scarce water resources, price elasticity and elasticity of demand.

4. Long-Term Supply

When the product is available over an extended period and its production capacity can be adjusted, it is referred to as long-term supply. For example, adequate power grids ensure there is a continuous supply of electricity to consumers, which can be adjusted based on consumer demand.

5. Market Supply

Market supply is the total quantity of goods offered by all producers at a given price over a specified period within a specific market. For example, all the paddy supplied by farmers in the APMC market at a minimum support price(MSP) set by the government during a harvest season.

What is the Law of Demand?

In contrast to the law of supply, the law of demand states that there is an inverse relationship between the price of goods and the product demand in the market. When the product price decreases, there is an increase in product demand and vice versa – assuming that all other factors like customer choice, earnings and price of alternate products stay the same.

The law of demand is graphically represented using demand curve and demand schedule, showcasing the relationship between product price and product demand. Aggregate planning, an effective technique to anticipate demand, helps business owners to align their production, manpower and warehousing requirements.

What is the Difference Between Law of Demand and Law of Supply?

| Law of Demand | Law of Supply | |

| Definition | As the price of a good increases, the quantity demanded decreases | As the price of a good increases, the quantity supplied increases |

| Direction of Relationship | Inverse relationship between price and quantity demanded | Direct relationship between price and quantity supplied |

| Factors Held Constant | Assumes all other factors affecting demand (income, preferences, prices of substitutes and complements) remain constant. | Assumes all other factors affecting supply (technology, input prices, number of suppliers) remain constant. |

| Demand Curve | Downward sloping from left to right. | Upward sloping from left to right. |

| Substitution Effect | Lower prices increase purchasing power, leading to more demand. | Higher prices increase profitability, leading to more supply. |

| Income Effect | Lower prices increase real income, leading to more demand. | Higher prices increase profitability, leading to more supply. |

| Market Behavior | Customers buy more as prices decrease | Producers supply more as prices increase |

How is Equilibrium Price Achieved?

Equilibrium price is the product price determined by the market when the amount of product supplied is equal to the product demand. When there is excess demand, the price of a product increases to restore equilibrium. On the other hand, when there is excess supply, the price tends to decrease.

Simply put, the equilibrium price indicates market efficiency where resources are allocated optimally based on customer preferences and manufacturer capabilities. The price undergoes constant adjustments in response to changes in demand and supply in the market, ensuring market stability over time.

You May Like: What is Breakeven Point?

Four Basic Laws of Supply and Demand

1. Increased Demand, Unchanged Supply

In a scenario when there is a constant product supply, any increase in product demand would create product shortage in the market, driving its price upwards.

2. Decreased Demand, Unchanged Supply

When the supply is constant, a decrease in demand will lead to surplus products in the market, pulling the price of the product downwards.

3. Increased Supply, Unchanged Demand

When the demand is constant or stable, an increase in production will lead to oversupply, pulling the price of the product downwards.

4. Decreased Supply, Unchanged Demand

When the demand is constant or stable, a decrease in supply leads to product scarcity, pushing the price of the product upwards.

| Supply | Demand | Price | Result |

| Unchanged | Increased | Increases | Product Shortage |

| Unchanged | Decreased | Decreases | Product Surplus |

| Increased | Unchanged | Decreases | Product Surplus |

| Decreased | Unchanged | Decreases | Product Shortage |

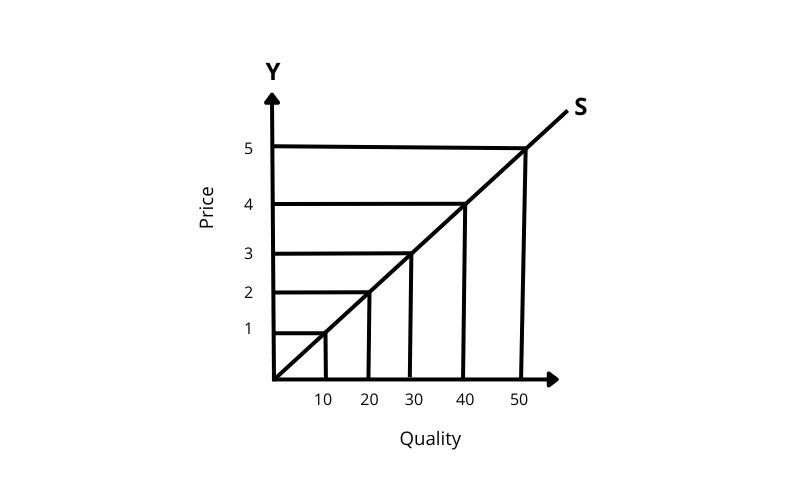

Law of Supply Curve

The supply curve is used to state the law of supply graphically, which says that a higher price of goods leads to a higher supply of goods because the producer is inclined to produce more and earn more revenue until the profit maximization objective is fulfilled. The same relationship is represented in the law of supply diagram, which slopes upward from left to right.

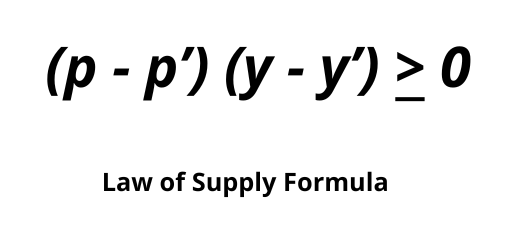

Law of Supply Formula

To explain the law of supply, we can also use the formula given below.

Where

p = price of product when quantity of supply is y

p’ = price of product when quantity of supply is y’

y = quantity of product supplied in market at price p

y’ = quantity of product supplied in market at price p’

According to the law of supply equation (p – p’)(y – y’) >= 0, if there is a change in product price, the amount of supply changes proportionally. So, if there is any increase in product price i.e. p > p’, then the product supply also increases y > y’. Similarly, if the product price decreases p < p’, then its supply also decreases y < y’. This shows a positive relationship between price and supply, which is also represented in the supply curve.

Exception of Law of Supply

Economies of Scale

Large-scale production or changes in business strategy can alter the quantity of product supplied irrespective of price fluctuations.

Market Dominance

When a single or a few businesses control the market, product supply can be controlled irrespective of traditional supply-demand dynamics.

Competition

Strong competition in the market can compel suppliers to increase supply even if product prices are falling.

Perishable Goods

Products with limited shelf lives may see increased supply regardless of price fluctuations.

Unique Production

Goods that are unique in design or produced in limited quantities do not adhere strictly to typical supply laws. eg. a custom-made machinery

Inelastic Supply

The supply of certain products like oil cannot be suddenly increased in response to changes in price. Drilling new wells and exploring new oil fields require significant time and investment.

Wrapping Up

Law of supply is a commonly used theoretical concept explaining how the product price determines the number of goods supplied in the market. When the product price increases, the producers are motivated to produce more to earn more profit by increasing the supply of product.

Understanding the law of supply helps in developing strategies to efficiently manage supply and quickly respond to market situations. Sage X3 ERP is a powerful tool that helps business owners to streamline their production output and efficiently meet customer demand.

FAQs

1. What is the Law of Supply Definition?

Law of supply meaning is that it is an economic concept that represents a relationship between product price and quantity of product supplied, which explains that as the price increases, the quantity supplied also increases.

2. What is the Law of Supply Diagram?

It is a graphical method to depict the relationship between the price of a product and the supply of the product in the market.

3. Define Law of Supply

According to the law of supply, when the product price rises, its quantity supplied by producers also rises, assuming all other parameters remain the same.

4. What is the Difference Between Law of Demand and Law of Supply?

The law of demand represents the relationship between product price and product demand by customers whereas the law of supply describes the relationship between product price and product supply by manufacturers.

5. What is the Law of Supply Example?

A good example of law of supply is when a manufacturer increases the production of leather shoes from 10,000 to 13,000 units in response to the increase in its price from Rs5000 to Rs8000, to cater to higher demand and earn more revenue.